Weekly Market Intelligence Brief — February 22, 2026

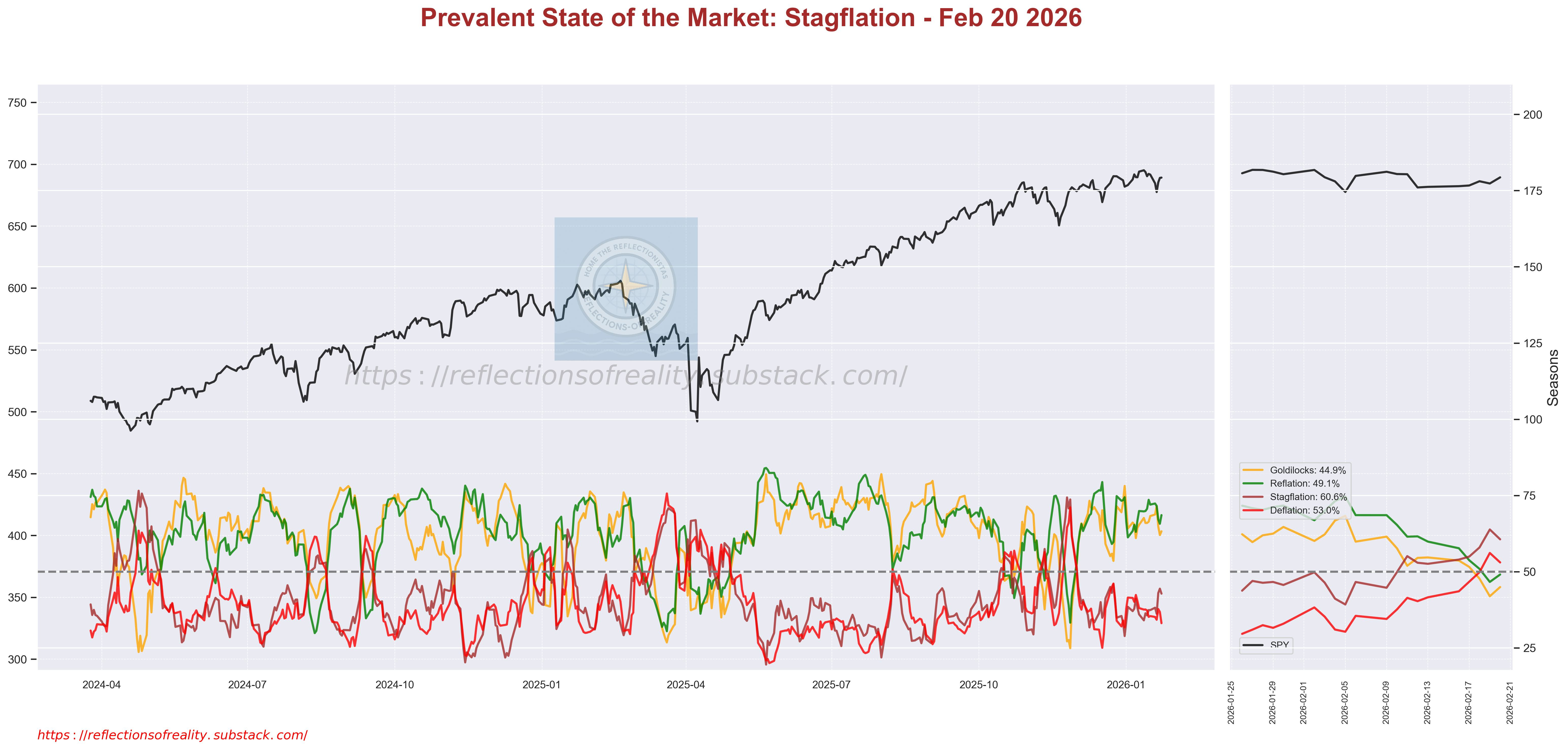

🎭 Theme of the Week: Stagflation Prevails Amid Rotational Shifts

Strong accumulation flows into cyclicals and consumer sectors indicate persistent momentum despite broader concerns.

Rotation into growth-oriented tech and biotech assets counters the dominant risk-off regime.

Overvaluation pressures and weak market breadth create tension, amplifying risks of divergence resolution.

📰 Key Market Influencing News (Last Week)

Supreme Court ruled 6-3 on Friday to strike down Trump’s broad IEEPA-based global tariffs as unauthorized, leading to stocks rallying on relief from trade uncertainty and potential consumer price pressures; Trump immediately imposed a new 10% temporary global tariff (later hiked) under alternative authority, sustaining policy volatility.

Federal Reserve minutes from January revealed uncertainty on future rate cuts, yet S&P 500 advanced led by AI stocks like Nvidia.

Mixed trading in major indexes, with software sector declines offsetting gains in other areas.

Shift toward value stocks noted in early 2026 insights, influenced by political and economic developments.

Trump tariff ruling impact on Friday’s market

On Friday, February 20, 2026, the Supreme Court ruled 6-3 to strike down most of President Trump’s broad global tariffs imposed under IEEPA emergency powers, deeming them unauthorized. This triggered a relief rally in stocks, with major indexes closing higher (S&P 500 +0.6-0.7%, Nasdaq +0.9%, Dow +0.5%) as trade-exposed sectors benefited from reduced uncertainty around inflation and consumer costs.

However, Trump quickly responded by imposing a new temporary 10% global tariff (later raised) under different authority, tempering gains and reintroducing policy volatility. This fits the “Trump’s renewed TAX chaos” theme (tariffs as import taxes) and contributed to whipsaw sentiment during the FEB OPEX close.

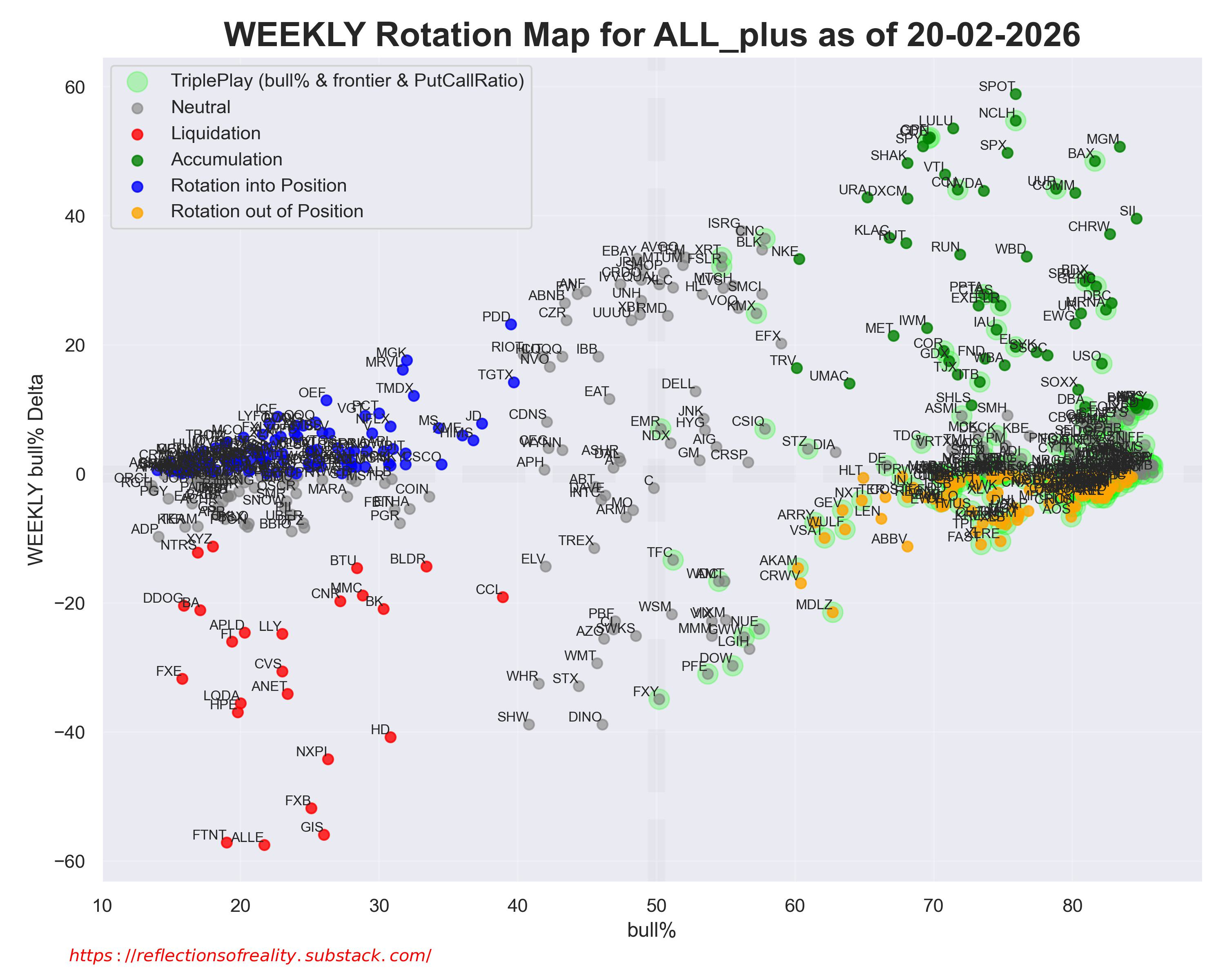

🏛️ Stock Quadrant Overview

🟢 Accumulation

SPOT +58.9 [🚀] → Streaming demand and ad revenue drive subscriber growth.

NCLH +54.8 [🚀] → Travel rebound boosts cruise bookings and occupancy rates.

LULU +53.6 [🚀] → Fitness trends fuel athleisure sales and e-commerce expansion.

GPN +52.2 → Digital payments surge amid cashless economy shift.

CDE +52.0 → Industrial silver demand rises with electronics and green tech.

🔵 Rotation into Position

PDD +23.2 → Chinese stimulus supports e-commerce consumption recovery.

MGK +17.6 → Mega-cap growth draws flows on AI and innovation themes.

MRVL +16.2 → Semiconductor demand from data centers and AI chips.

TGTX +14.2 → Oncology pipeline progress attracts biotech interest.

TMDX +12.1 → Organ transplant tech expands in medical device sector.

🔴 Liquidation

ALLE -57.5 → Security firms face sell-off from economic slowdown fears.

FTNT -57.1 → Cybersecurity competition pressures lead to position unwinds.

GIS -55.9 → Consumer staples shift due to changing food preferences.

FXB -51.8 → UK currency weakened by ongoing economic challenges.

NXPI -44.2 → Auto chip demand softens amid industry headwinds.

🟡 Rotation out of Position

XLB -7.8 → Materials face cyclical slowdown and commodity volatility.

WULF -8.6 → Crypto mining trimmed on energy costs and regulation risks.

TPL -8.9 → Oil royalties volatile amid energy transition concerns.

VSAT -9.9 → Satellite broadband competition prompts outflows.

XLRE -10.4 → Real estate sensitive to interest rate expectations.

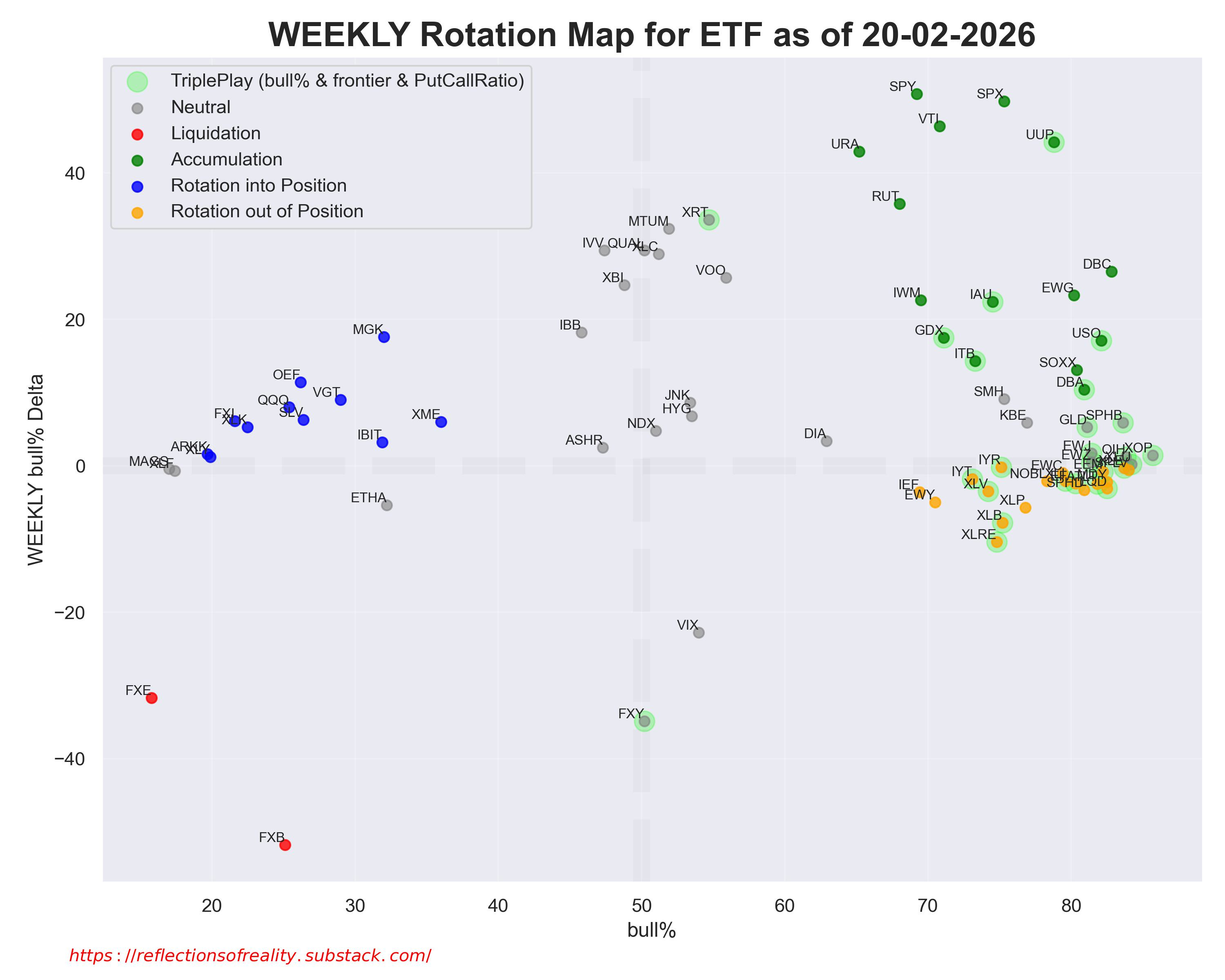

📊 ETF Quadrant Overview

🟢 Accumulation

SPY +50.8 → Broad market resilience amid economic data strength.

SPX +49.8 [🚀] → Index flows supported by corporate earnings stability.

VTI +46.4 [🚀] → Total stock exposure benefits from diversified rallies.

UUP +44.2 [🚀] → Dollar strengthens on safe-haven and policy divergence.

URA +42.9 → Uranium demand rises with nuclear energy focus.

🔵 Rotation into Position

MGK +17.6 → Growth mega-caps positioned for tech innovation cycle.

OEF +11.4 → Blue-chip stability attracts amid market rotations.

VGT +9.0 → Tech sector nibbles on AI and software advancements.

QQQ +8.0 → Nasdaq rebound draws selective growth interest.

SLV +6.3 → Silver as inflation hedge in uncertain macro.

🔴 Liquidation

FXB -51.8 → British pound sold off on UK growth concerns.

FXE -31.7 → Euro weakened by EU economic and policy headwinds.

🟡 Rotation out of Position

EFA -2.4 → International developed markets trimmed on global risks.

TLT -2.5 → Long Treasuries reduce amid rising yield expectations.

LQD -3.1 → Corporate bonds face outflows from rate volatility.

SPHD -3.3 → High dividend strategies rotate to growth preferences.

XLV -3.5 → Healthcare profit-taking after sector outperformance.

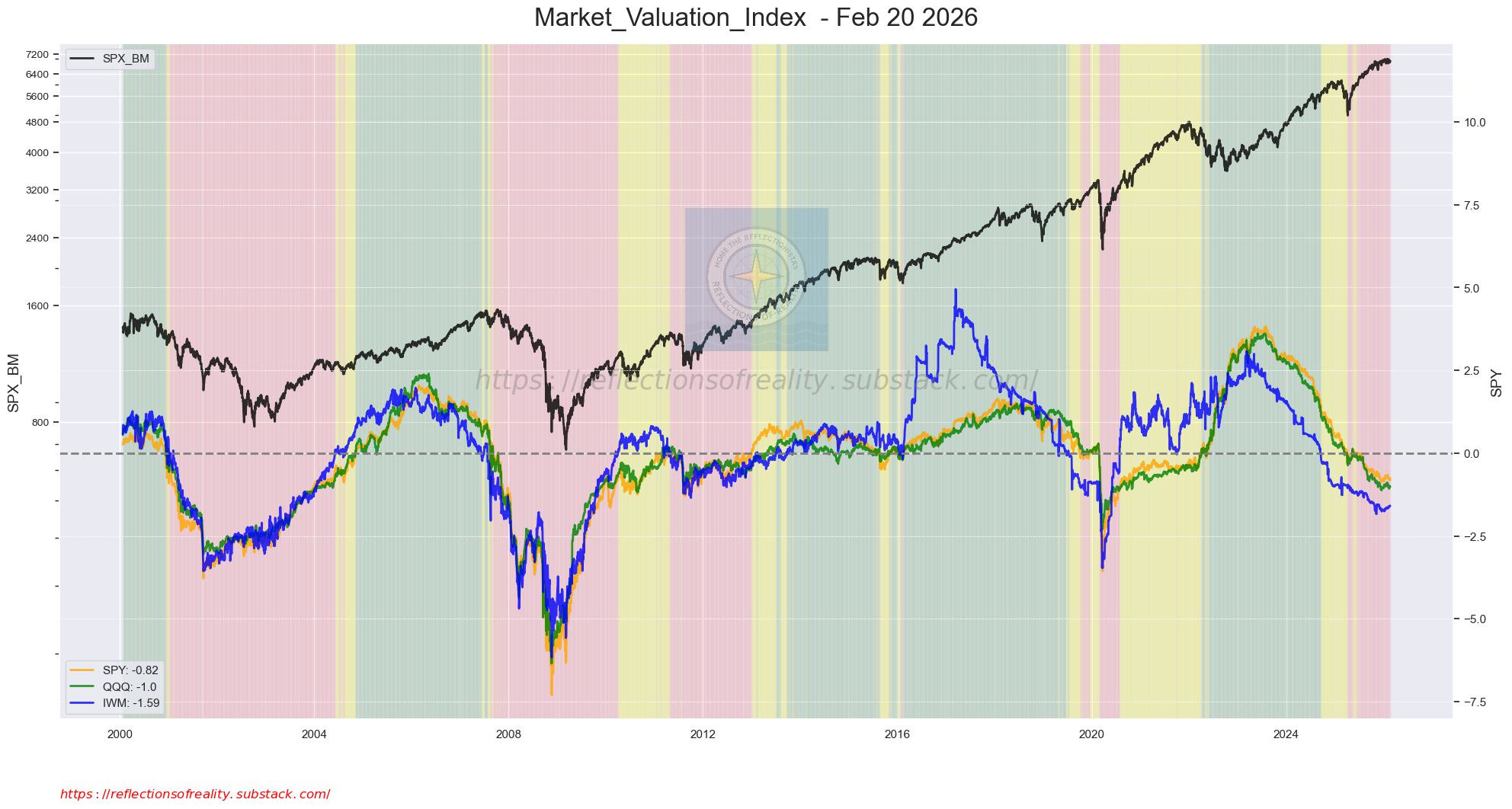

🌐 Macro Regime & Valuation Context (February 22, 2026)

📈 Market Valuation Index (MVI) – Medium- to long-term valuation view: SPY -0.82 🔴 | QQQ -1.0 🔴 | IWM -1.59 🔴 → all red, medium-term overvaluation; small-caps most stretched.

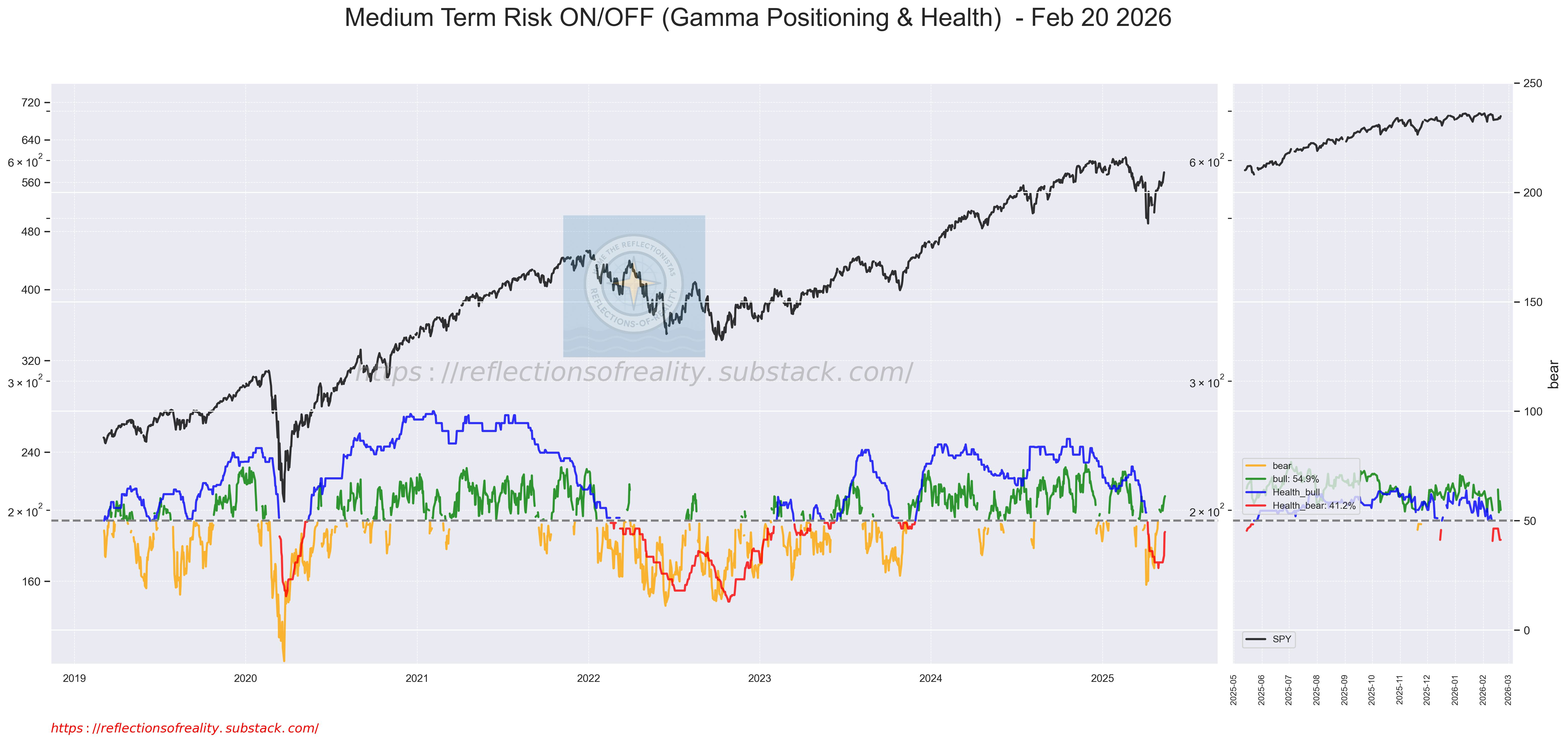

💹 Medium-Term Risk ON/OFF – Medium-term flow & positioning:

Bull 54.9% 🟢 + Health_bull 41.2% 🔴 → mixed signal with bullish positioning but weak breadth.

⚠️ MVI vs. Medium-Term Risk ON/OFF Discrepancy:

In a healthy market both are aligned in a bullish way; MVI can diverge from Medium-Term Risk ON/OFF, but this is a clear bubble warning sign that will require resolution through stock market correction, lower interest 10Y TSY rates or higher earnings.

🌤️ Seasons – Short- to medium-term leadership & composition:

Stagflation 60.6% 🔴 (Deflation 53.0% 🔴) → dominant short-term risk-off with stagflation bias; examples from quadrants include gold and commodities in accumulation. Macro Regimes (Seasons) need to align as well but can lag for a while in a healthy market; divergence = increased risk.

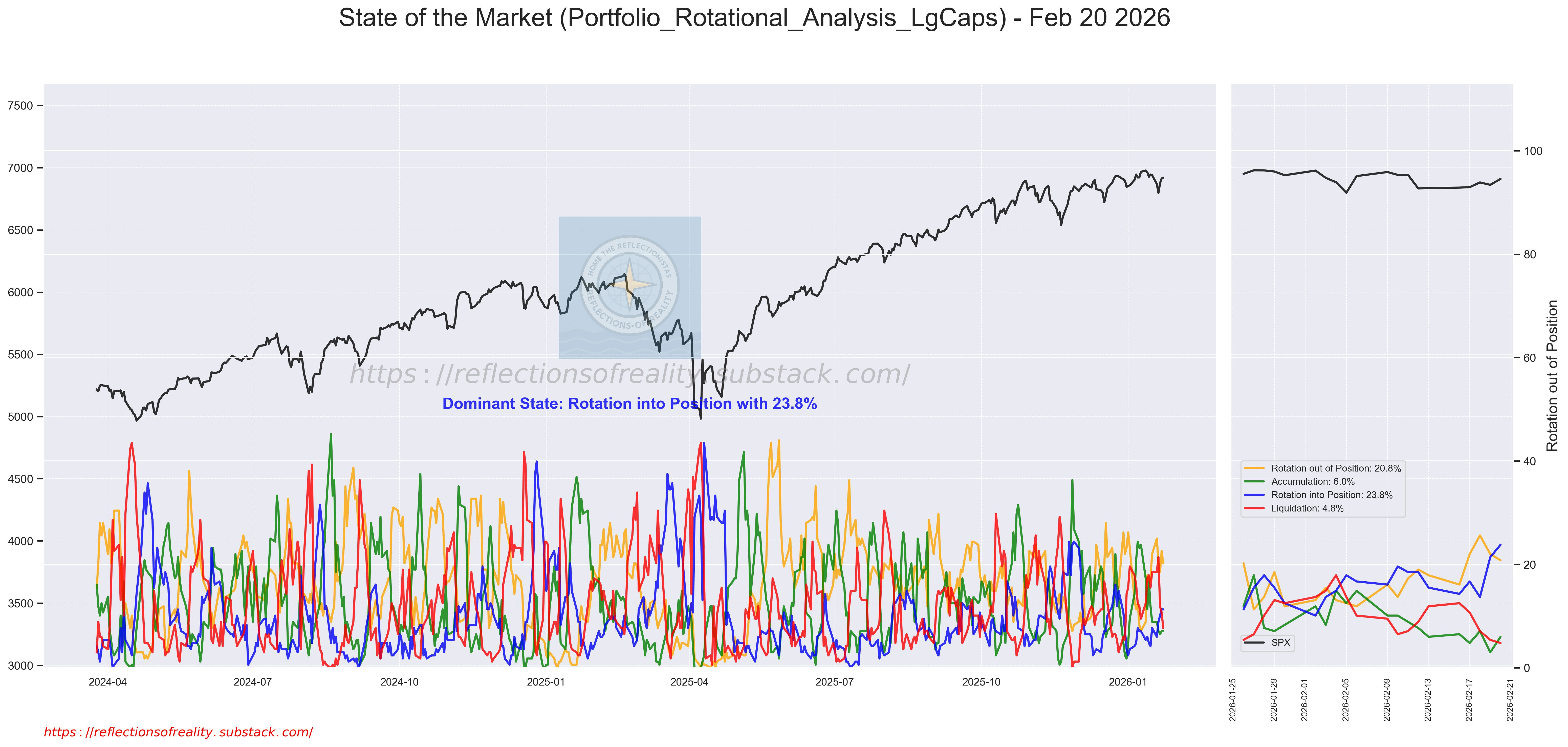

🔄 Portfolio Rotation (LgCaps) – Short- to medium-term flow dynamics:

Rotation into Position 23.8% 🔵 dominant → still bearish but cautious nibbling.

Cross-context ⚡:

Short-term stagflation dominance (Seasons chart showing ~60.6% stagflation leadership) contrasts sharply with the mixed medium-term gamma signals (Bull positioning at 54.9% yet weak Health_bull at 41.2%) and persistent long-term overvaluation across indices (MVI all negative, with small-caps most stretched at -1.59). This multi-timeframe divergence elevates bubble risks and increases the probability of a corrective unwind to realign signals.

On the tactical side, Friday’s February OPEX expiration closed on a bearish intraday tone that shifted to a bullish finish amid relief from the Supreme Court tariff ruling—major indexes ended firmly higher (S&P 500 +0.7% to ~6,909, Nasdaq +0.9%). This sets up a fair chance for bullish re-ignition in the post-OPEX window, provided news flow remains contained and doesn’t derail the setup (particularly Trump’s rapid reimposition of a new 10-15% global tariff under alternative authority, fueling renewed “TAX chaos” uncertainty). Monitor closely for any escalation that could flip sentiment back to risk-off.

Conclusion 🎯: Favor cautious nibbling in rotational opportunities while hedging overvalued segments and monitoring regime alignment.

Quick Glossary

bull% — Positioning & Flow Trend Indicator (full explanation + live charts: https://reflectionsofreality.substack.com/p/access-to-our-bull-charts)

MVI — Market_Valuation_Index or Equity Valuation Pressure Index (full explanation: https://reflectionsofreality.substack.com/p/market_valuation_index)

Medium Term Risk ON/OFF — Avg. lg. Cap Price Positioning within the Call-Put-Frontier Range

Medium Term Risk ON/OFF: Health — lg. Cap Market Breadth of medium term Machine Learning model

Macro Regimes — “Seasons”: Goldilocks: Strong growth, low inflation → best: stocks/tech/credit | worst: USD/vol/gold Reflation: Rising growth, rising inflation → best: cyclicals/commodities | worst: bonds/defensives Stagflation: Weak growth, high inflation → best: defensives/gold/vol | worst: equities/credit Deflation: Contracting growth, falling inflation → best: bonds/USD | worst: stocks/commodities

Legend

[🚀] = Bull Trendfollowing Triggered (only in Accumulation if bull% >50%)

🟢 + 🟡 = Risk-On | 🔴 + 🔵 = Risk-Off

❤️ Support our Work

📢 Stay Connected & Support

We provide intra-week updates via:

🔔 Substack Notes

💬 Community Chat